17 December 2020

Is the time right for negative rates in the UK?

David Aikman and Francesca Monti

The economic crisis triggered by the Covid-19 pandemic, coupled with historically low interest rates and persistently low inflation, is prompting a rethink of central banks’ toolkit globally.

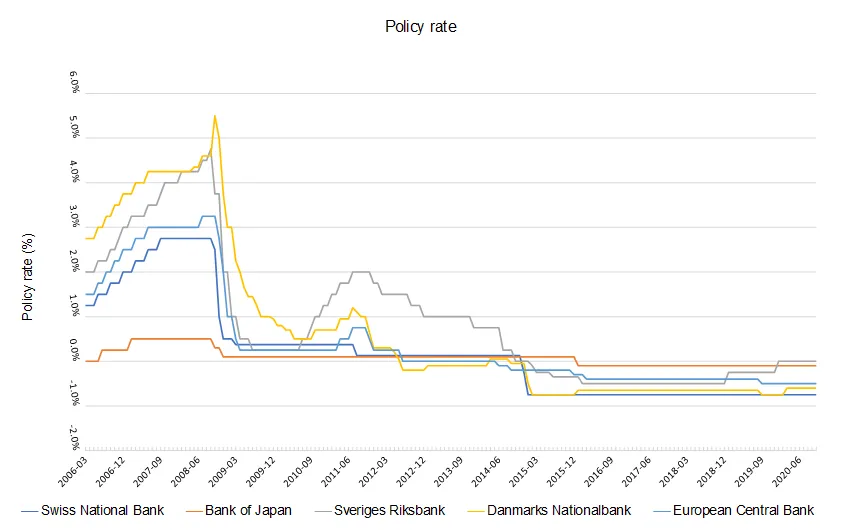

In the UK, in the last decade, the Monetary Policy Committee (MPC) has discussed the opportunity of rates venturing in negative territory on several occasions. In 2016, after the Brexit Referendum, when the MPC deployed an expanded set of unconventional tools, it deemed that the effective lower bound on the nominal rate was “close to, but above zero per cent”. Since then, a growing number of central banks – the Sverige Riksbank, Danmarks Nationalbank, the Swiss National Bank, the European Central Bank and the Bank of Japan – have set negative nominal interest rates.

With the Covid-19 pandemic putting further strain on policymakers’ arsenal, the idea of negative rates has gathered further support. For example, external MPC member Gertjan Vlieghe voiced cautious support for the idea in a recent speech on 20 October 2020 and external MPC member Silvana Tenreyro pointed to “encouraging” evidence from other countries (in an interview in the Sunday Telegraph, 26 September 2020). The idea of negative rates remains controversial on the MPC, however, with internal members highlighting implementation challenges (see Dave Ramsden interview on 21 October 2020).

Interestingly Overnight Index Swap rates 12 months out have been negative since May 2020 (at 30 November, the 12-month ahead forward rate is -0.02 per cent), suggesting that financial markets expect Bank Rate to dip below zero.

In this blog we discuss the costs and benefits of negative interest rates and, based on theory and the growing body of empirical evidence, we give our opinion on where the balance of this trade-off lies.

The theory

Is negative interest rate policy (NIRP) effective and are there limits to this effectiveness? In principle, in a world without cash or if policymakers could take measures to avoid the hoarding of physical currency, there would be no “lower bound” on the interest rates that can be set by central banks. There would be nothing special about setting a negative rate in such a world (Lilley and Rogoff, 2019). With paper currency in circulation, however, households and companies avoid the negative return on deposits by holding cash instead, rendering the policy ineffective. John Maynard Keynes dubbed this a “liquidity trap”.

But what exactly is the lower bound on rates? Banks, other companies and households with very large deposits are potentially willing to pay something for the storage and liquidity services provided by reserves and deposits, so the lower bound on rates might be lower than zero. Based on evidence from Sweden, Eggertson et al. (2019) suggest that there are two bounds: a “policy rate bound,” at which the banks would rather hold paper currency than reserves, and a “deposit rate bound,” which instead affects retail household deposits. They find that the pass-through in Sweden remained relatively unchanged until the policy rate reached -0.25 per cent.

They also find that lending rates do not respond to policy cuts once the deposit lower bound is reached, especially those offered by banks that rely more heavily on deposits for their financing. The authors develop a model to show that the impact of negative policy rates on bank profits is a sufficient statistic for the qualitative impact of negative policy rates on bank lending. The intuition is that bank profits increase if the effective pass-through of negative policy rates is larger to bank liabilities (including deposits) compared to bank assets (including lending).

Another explanation for why interest rate cuts can weaken banks’ ability to lend is proposed by Brunnemeier and Koby (2019). They develop a model in which what they call the “reversal interest rate” i.e. the rate at which interest rate cuts stop boosting the economy is endogenous and depends on the size of the banks’ maturity transformation. The intuition is that an interest rate cut affects banks’ net worth in two opposing ways. The capital gains the bank makes on assets with long-term fixed-rate coupon payments (e.g. bonds) are offset by the impact the rate cut has on banks’ future net interest income. If the latter effect dominates, banks’ net worth falls, making the capital constraint they face more proximate. When this constraint binds, banks charge higher lending rates in order to decrease their leverage. The reversal rate in this setting can be positive or negative and depends on the size of the capital gains, the overall capitalisation of banks, and the deposit supply elasticity.

Even if banks do not pass on negative interest rates to households and firms and their capital positions are weakened by the squeeze of the interest margins, De Groot and Haas (2020) suggest another channel through which lower rates can still be expansionary: the signalling channel. By setting negative policy rates, a central bank signals lower-for-longer rates, especially when there is a lot of policy inertia. Even though current deposit rates do not change, the policy change generates an expansionary intertemporal aggregate demand effect, which can offset the contractionary effect of negative interest rates due to the interest margin channel.

The evidence

The existing empirical evidence on the effectiveness of negative interest rates is mixed.

Eggertson et al. (2019) use Sweden as a case study and find that, while the transmission of negative policy rate policy to money markets and other highly liquid assets, such as short-term government bonds, has been strong, the pass-through to lending rates fell substantially once rates fell below -0.25 per cent. This can be explained by Swedish banks’ reliance on retail deposit financing, the rates on which tend to be sticky at zero.

Heider et al. (2019) focus on the Euro area and also find that banks are reluctant to pass on negative interest rates to retail depositors. They study the effect of the introduction of negative rates by the European Central Bank (ECB) in 2014 on the supply of bank credit using a so-called “difference-in-difference" approach. They exploit the fact that the net worth of banks which rely heavily on retail deposits rather than market-based debt is hurt more because the decrease in rates does not transmit to lower funding costs for these banks. This adverse effect on their net worth leads the banks to lend to riskier borrowers while expanding the overall quantity of their lending by less than banks in the control group. A further finding is that these effects happen only when policy rates venture in negative territory; when rates are positive, the reliance on deposits is not relevant in determining the pass-through of rate changes to risk-taking and lending volumes.

A more optimistic take on the effectiveness of negative interest rates take comes from Altavilla et al. (2020) who also look at the negative interest rate policy implemented by the ECB in 2014. They find that sound banks, i.e. investment-grade and similar, have tended to pass on negative interest rates to corporate depositors without experiencing a contraction in funding. Their result stems from the fact that they focus on corporate deposits rather than those of households. The majority of household deposits are small sums so in the presence of negative rates, they can be withdrawn and held as cash. Companies instead need deposits to operate and many have accumulated significant deposit holdings over the past decade. Sound balance sheets appear to give banks a degree of market power, which allows them to pass through interest rates cuts to wholesale deposit rates without seeing a drain on deposits.

The authors also find that the transmission of NIRP is enhanced by the fact that firms with large cash-holdings exposed to negative rates decrease their liquid asset holdings and invest more.

In sum, the evidence suggests a reduction of policy rates into negative territory is more likely to be passed on through the banking system the smaller the fraction of household deposits in bank funding, the stronger the health of the banking system, and the larger the cash holdings of corporates.

The case of the UK

One issue that central banks worry about when considering setting a negative rate is its effect on the banking system. The concern is that there might be behavioural or even legal frictions which impede the pass-through of negative policy rates to loan and deposit rates in the banking system. Evidence from the euro area suggests that this concern is particularly acute for retail deposits, with banks being generally unwilling to pass on negative rates to household deposit accounts. For this reason, banks’ net interest margins are likely to be squeezed when negative policy rates are set, and the effect is likely to be more pronounced the larger the share of retail deposits in the bank’s funding base.

While this is a concern, our view is that such arguments should not prevent the Bank of England from setting a modestly negative Bank Rate. We say this for two reasons. First, household deposits make up a smaller share of UK banks’ funds than for their euro-area counterparts: household deposits are around 19 per cent of the UK banking system’s total liabilities but 30 per cent of that of the euro area banking system. So, any adverse impact on net interest margins for the UK banking system as a whole is likely to be smaller than that seen in the euro area.

Second, central banks have developed innovative ways of alleviating such adverse impacts – this may be particularly important for certain classes of intermediary that are highly reliant on deposit funding, such as building societies. Many central banks that have set negative policy rates have accompanied this with a system of tiering in the remuneration of reserves, with only excess reserves beyond a certain level carrying a negative rate. Another innovation is to provide term funding at a preferential rate to banks and building societies that is contingent on their continued lending to the real economy.

In this story

Advisor, Qatar Centre for Global Banking & Finance